Buying A Home: First Time Mortgage Tips (Pt 1)

If you are looking at buying a home in Charleston SC and it will be your first, the process can be intimidating. However, with a little knowledge and preparation, you can eliminate a lot of the stress.

Here are some first home buying tips Charleston SC to make the process much easier for you.

Here are some first home buying tips Charleston SC to make the process much easier for you.

One of the most important factors of buying your first home is the mortgage. This can be huge contributor to the stress of buying a home, but it doesn’t need to be.

By being proactive you can greatly reduce this stress, and focus entirely on the overall goal: finding the right house.

Your credit is a key component of qualifying for a mortgage.

Your credit is a key component of qualifying for a mortgage.

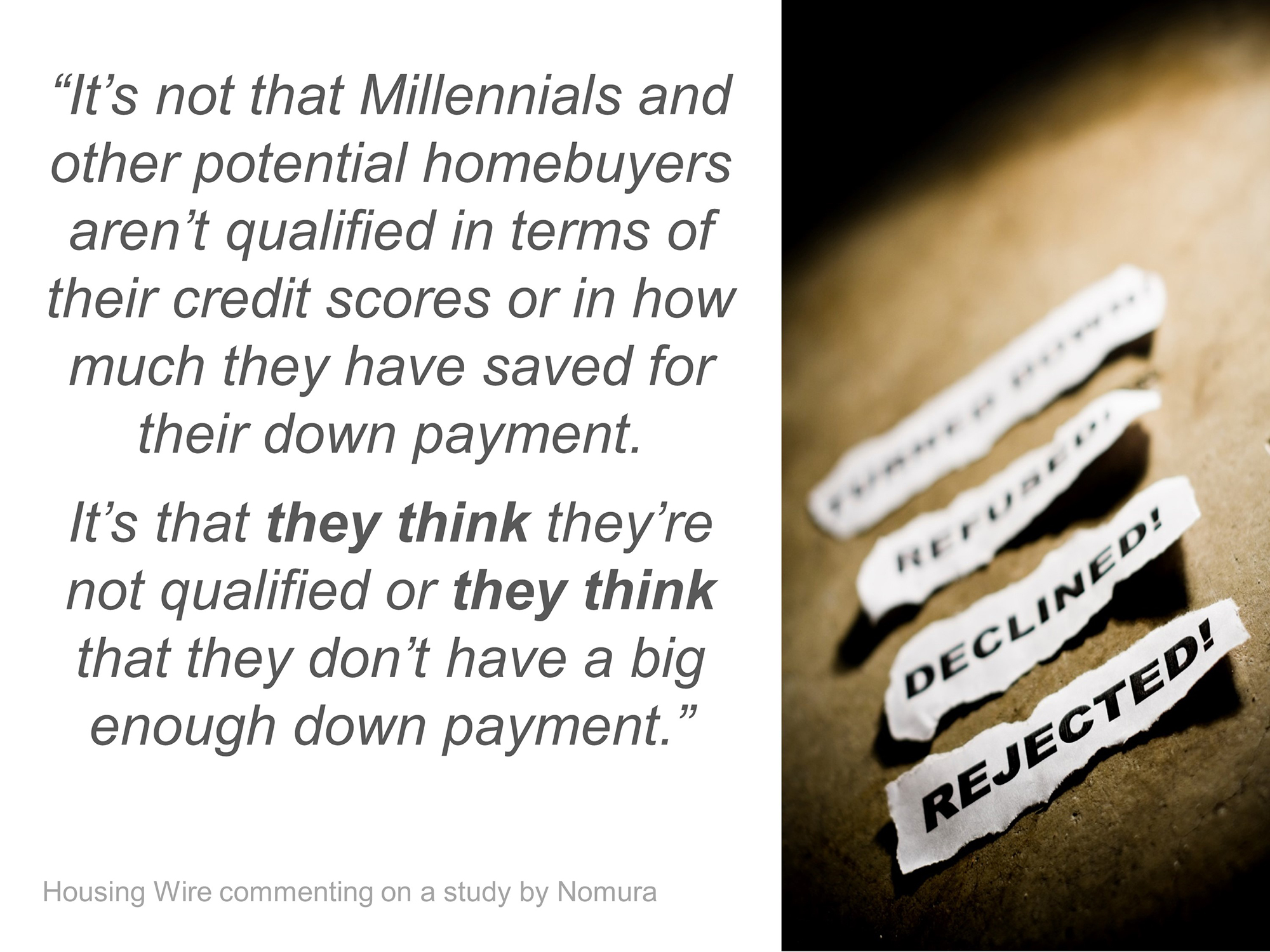

Don’t assume that your credit is fine.

In fact, recent surveys have found that the opposite is true–too many would be buyers don’t think their credit is good enough.

The best way to tell is to contact a mortgage loan officer and get pre approved.

This process doesn’t take but a few days, and costs you nothing.

Pre approval will let you know where you stand today, help determine your price range, what your monthly payment will roughly be, and any credit issues you may have.

Credit issues can be minor things that can keep you from qualifying for a lower interest rate.

Or, they could keep you qualifying altogether.

Whatever issues you uncover, the loan officer can show you the quickest and easiest ways to overcome these issues.

It could take a week or two, maybe a couple months. In some cases it might be 6 months to a year, but at least you will identify the issues and know how to attack them.

It is a good idea to get this pre approval as early in the process as you can–before you start to look at homes. This allows you time to explore all your mortgage options and work on any credit issues.

Plus, no home seller will look at an offer that does not come with a pre approval letter.

Here are some other important considerations when it comes to pre approval if you are buying a home:

1) You Have More Than One Credit Score

There are many places online you can get your credit score. You can also get copies of your credit report.

There are many places online you can get your credit score. You can also get copies of your credit report.

However, when a lender pulls your credit, they are pulling up reports and scores from all 3 major credit bureaus (Experian, Equifax, and Trans Union).

These reports will not be identical, and it is likely the scores won’t either.

Not all creditors report to all 3 bureaus, so some of your credit information may not appear on all 3 reports.

Each credit bureau has their own way of calculating your score, and although they are similar, they are not identical.

Plus, they are not using the exact same information to calculate your score. Therefore, you will not have just one score–you will have three.

They are usually somewhat close to each other, but it isn’t unusual to see them vary greatly.

When a lender is looking at your credit scores, they are looking at the middle score. So, if your three scores are 720, 735, and 793, then your middle score is 735, and that is what the lender will base everything off of.

2) Know Your Partner’s Credit Score

There is the possibility of having a significant other/spouse on the mortgage as well.

There is the possibility of having a significant other/spouse on the mortgage as well.

This is known as a co-borrower.

This can be beneficial because you are using two incomes to qualify, which will allow you to qualify for a bigger loan.

However, lenders want to know their middle credit score as well, and they will use the lower of the two middle scores.

If your middle score is like the example above, 735, and your partner’s middle score is 650, then the lender will use the 650.

This can make a huge difference in whether or not you qualify, as well as the interest rate. It could also keep you from qualifying for a better mortgage.

This is where talking with a loan officer can really benefit you and eliminate stress. They can analyze your situation and help you remedy credit issues.

3) Factor In All Costs

When looking online, you will find online calculators that can help you estimate your monthly payment. However, be aware that most of the time you will get what is known as a Principle & Interest payment.

This is your monthly mortgage payment, but it is not the whole picture.

You also have to factor in taxes and home owners insurance. These are usually due once a year in one lump payment.

However, typically your lender will take care of making these payments for you.

In exchange, they prorate the payment into monthly installments and add that to your Principle & Interest monthly payment.

Your loan officer and real estate agent can help you to estimate how much extra these will be each month.

If you are buying a home in Charleston SC, a rough figure to use as a guesstimate would be about $100/month for taxes and $150/month for homeowners insurance.

You also have other potential costs: HOA fees (these can be due monthly, quarterly, or annually), flood insurance (required for certain areas of Charleston), and Private Mortgage Insurance (PMI).

Private Mortgage Insurance is common for loans over 80% of the home’s value, which is the majority of loans to first time home buyers.

PMI adds an additional .5% to 1% of the total loan amount each year. On a $200,000 loan, that could mean an extra $1000 to $2000 each year.

While you may qualify to buy a $250,000 home, that doesn’t necessarily mean you should buy a $250,000 home.

Your loan officer can help you factor in all costs and find out what you are comfortable with for a monthly payment. This will determine your true price range.

The rule of thumb is you do not want your monthly mortgage payment to be more than 30% of your gross monthly income.

Stay tuned as I finish my list of first home buying tips Charleston SC tomorrow. If you are looking at buying a home in the greater Charleston SC area, then visit my Pam Marshall Realtor website.

Leave a Reply