With the real estate bubble from 2008 still fresh in many American’s minds, people believe that we are heading towards another real estate bubble in 2017.

Rising home values have hit or exceeded their pre-crash peaks in many markets, fueling fears that we are just around the corner from another crash.

According to a recent report, the Modern Homebuyer Survey from ValueInsured, 58% of homeowners think that there will be a housing bubble and price correction in the next 2 years.

However, fears of another real estate bubble bursting are unfounded.

Home values approaching or exceeding previous highs are not the only factor that led to the market crash previously.

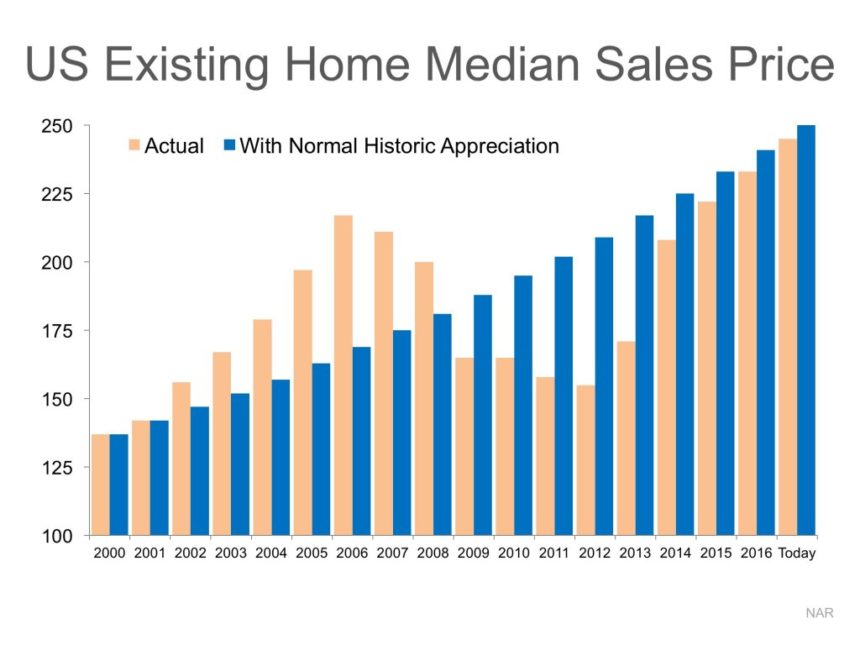

A look at the historical average appreciation for real estate shows that on an annual average, real estate appreciates at about 3.5% a year.

The last market that lead to the crash was itself an anomaly, as was the resulting crash.

If you take the big build up and crash out of the equation you see that the market is actually following the trend it would have followed by historical norms.

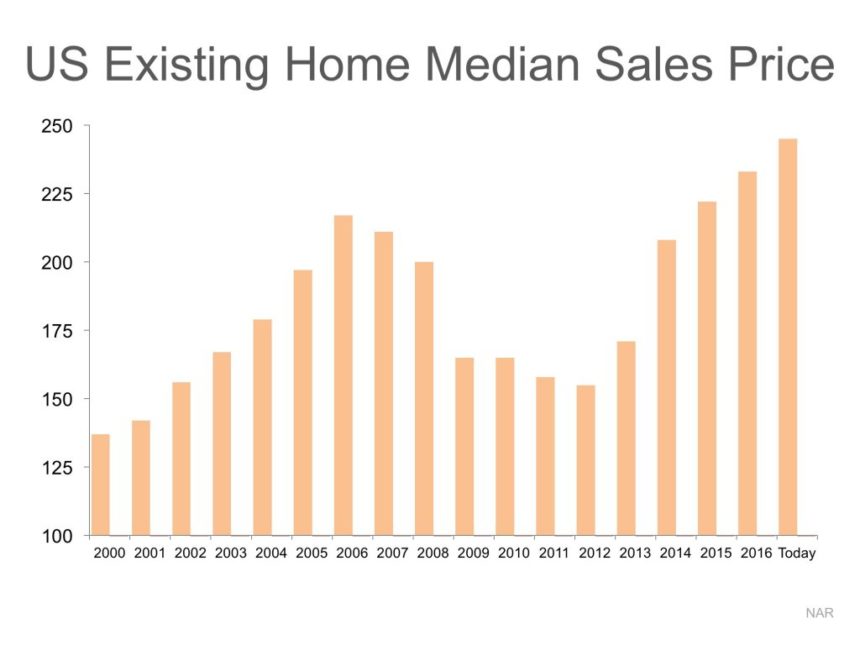

To better understand this, take a look at the following infographics. The first shows the median home value in the US since 2000:

This next infographic superimposes what the median home values would look like if the build up and crash had never happened.

In other words, if real estate had continued along at historical norms:

In other words, the market would be exactly where it is today, were it should be.

The Tale Of Two Markets

The market in 2007 was completely different than the current market.

There were many factors that contributed to the last crash, and these factors are not present in today’s market.

Here is a closer look at the difference between the two markets, and 6 reasons we are not heading for a housing market crash anytime soon.

1. Oversupply Of New Construction Homes

One factor that led to the previous crash was the overbuilding of new homes. Simply put, builders built too many homes.

There was an artificial demand created by far too lenient lending standards, which meant that many people were able to get approved for a mortgage that had no business being approved (more on that in a minute).

Builders built at a pace that far exceeded historical norms, and this led to an oversupply of homes.

In today’s housing market, things are vastly different.

The demand for housing is real, and it is not made up of buyers that should not be able to obtain a mortgage.

Builders are trying to catch up to the demand, but so far, they haven’t been able to.

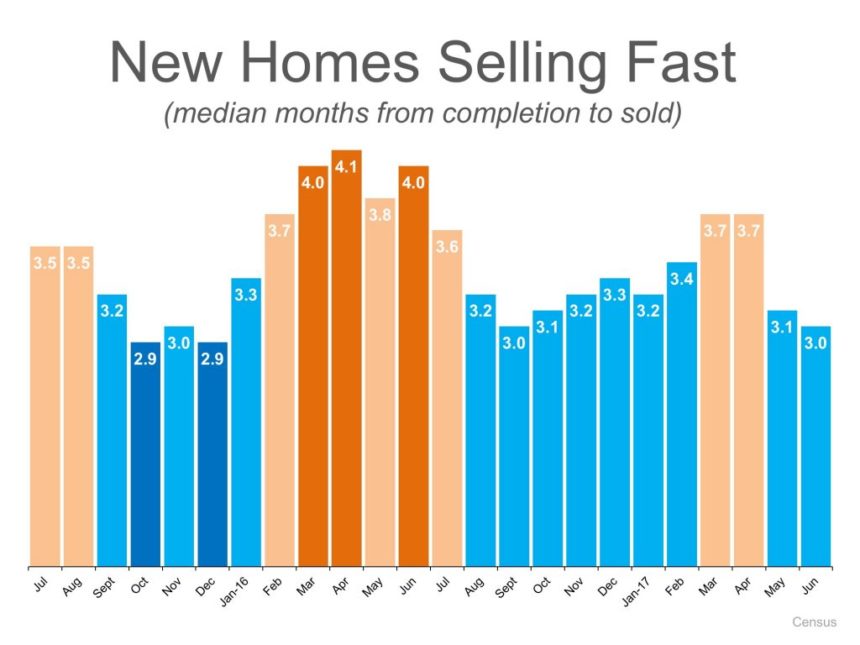

The latest Average Days On The Market for New Construction homes numbers show that demand still far exceeds the supply:

There are several challenges facing builders in trying to catch up to the demand, and I covered them in greater detail in a previous post.

But the fact remains that new construction homes aren’t keeping up with the demand.

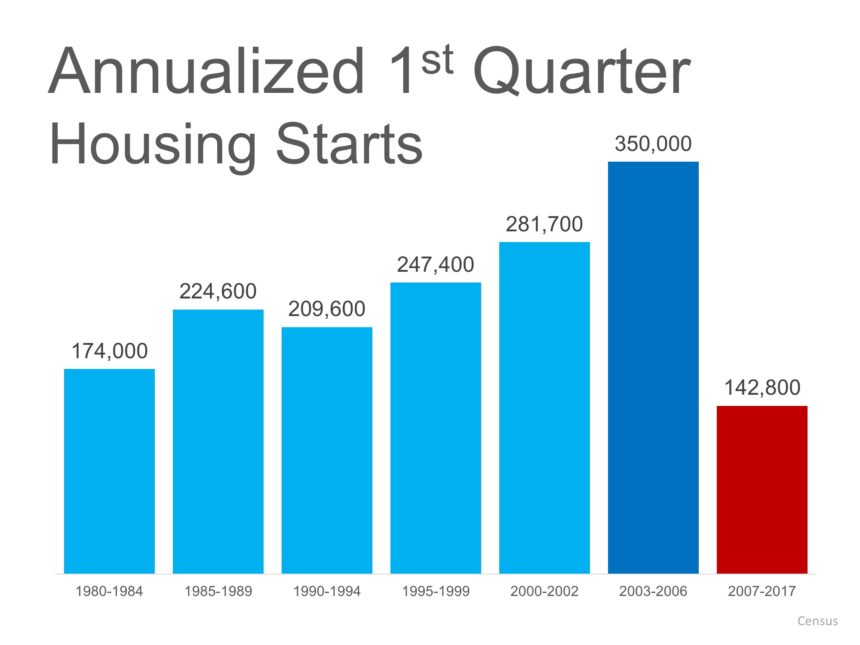

In fact, new construction starts haven’t even caught up to their historic norms:

Nationwide we are seeing the fewest new construction home starts going back to 1980.

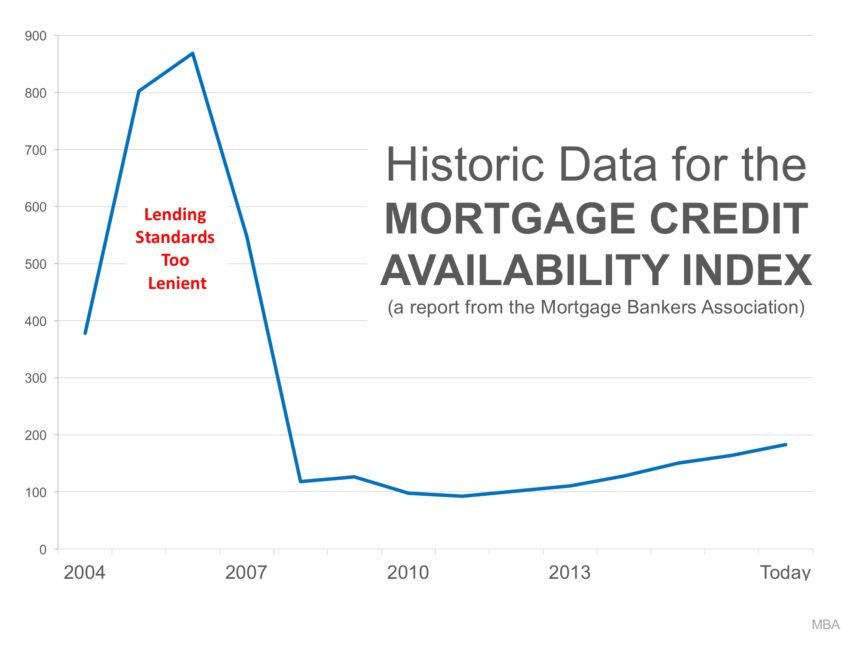

2. Loose Lending Standards Created The Real Estate Bubble

Leading up to the last real estate crash, lenders couldn’t give mortgages away fast enough. Pretty much everyone got a mortgage.

That may be a slight exaggeration, but the running industry joke in those days was that “if you could fog a mirror, you got a loan”.

Loose lending standards led to too many unqualified buyers getting a mortgage approval, and this artificially inflated demand.

After the crash, lenders tightened up their lending standards to an extreme.

It was virtually impossible to get a mortgage unless you had near perfect credit.

This certainly didn’t help the recovery process.

Lenders finally started to relax the standards just enough–enough to allow worthy borrowers to get mortgages.

But, they learned a brutal lesson last go round, with the proliferation of foreclosures and short sales, that they aren’t going back to the crazy days of everyone getting a mortgage.

This following infographic shows that over the last couple years lenders have loosened up the standards a reasonable amount, without getting anywhere near where they were during the early 2000s:

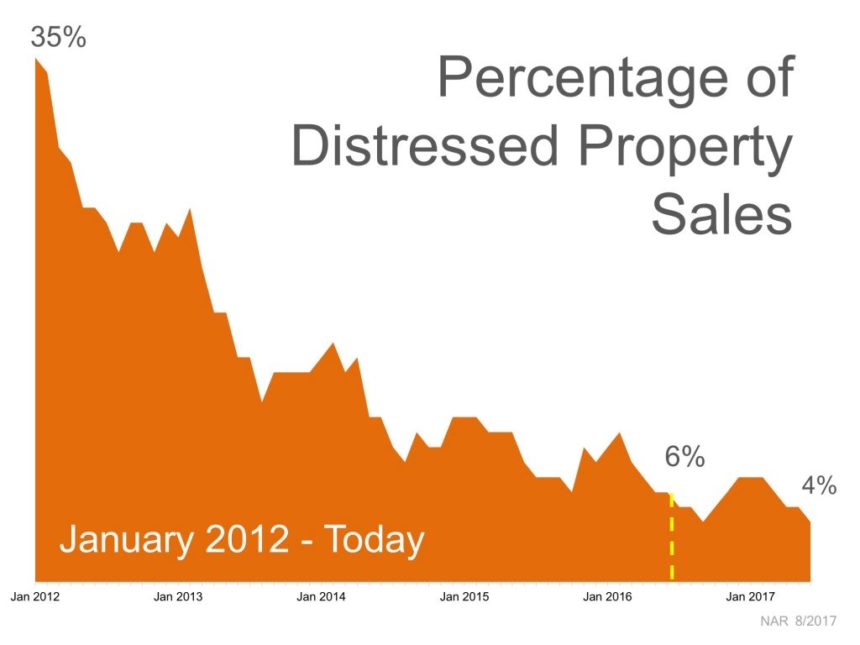

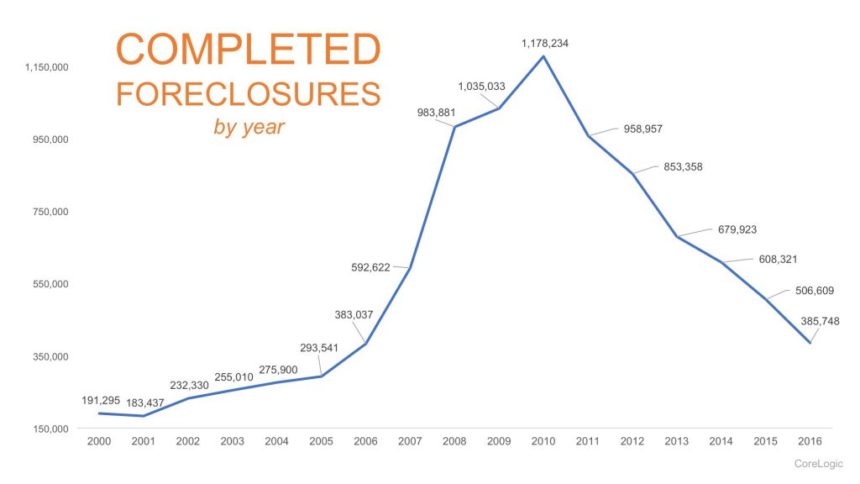

3. Unqualified Buyers Led To Defaults

As a result of loose lending standards, many otherwise unqualified buyers were approved for mortgages.

It wasn’t too long before these buyers started to miss mortgage payments. This led to the foreclosure crisis.

Foreclosures flooded the market. These homes went back on the market at a discounted price.

As a result, they impacted surrounding home values, and brought down overall home values.

This in turn led to short sales, which further depressed the market.

The number of distressed properties skyrocketed beyond normal market numbers, and contributed to the real estate market bubble bursting.

Distressed properties are not an issue in the current market.

For one, mortgages have gone to qualified buyers that are able to handle the financial responsibility that comes with home ownership.

The number of distressed sales have been sharply declining, and are close to reaching levels prior to the real estate market boom:

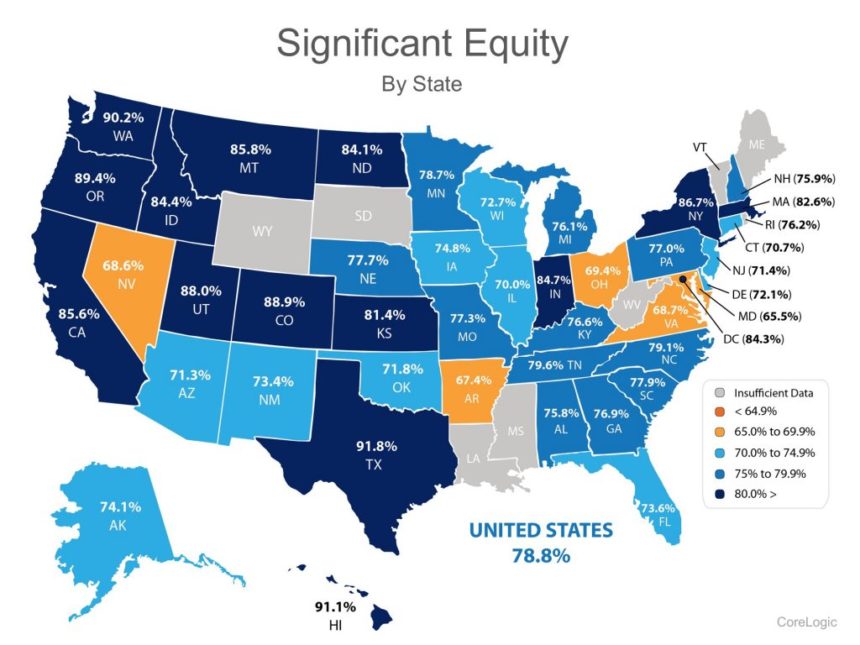

One benefit of the housing market recovery is that rising home values have helped many home owners that were in a negative equity situation climb out of that hole.

In fact, the majority of home owners in the US now have significant equity (greater than 20%) in their homes:

4. Strong Buyer Demand

As I mentioned earlier, the last market was fueled by artificially created demand. That is not the case in the current market.

Demand is strong, but supply is not keeping up. It is simple economics, when demand exceeds supply, prices go up.

Inventory of homes for sale are not only not keeping up to demand, but they are at historically low levels.

This in turn is driving home values up.

Inventory levels have actually hit 30 year lows:

Many home owners may not realize how much equity they have in their homes as a result of rising home values.

But a bigger problem is the fears of another crash looming.

It’s too bad they do not realize the opportunity that exists, because they are missing out and it is affecting the market.

So not only is demand strong right now, but there is another segment of would be buyers that would be actively in the process of purchasing a home if there were more homes available.

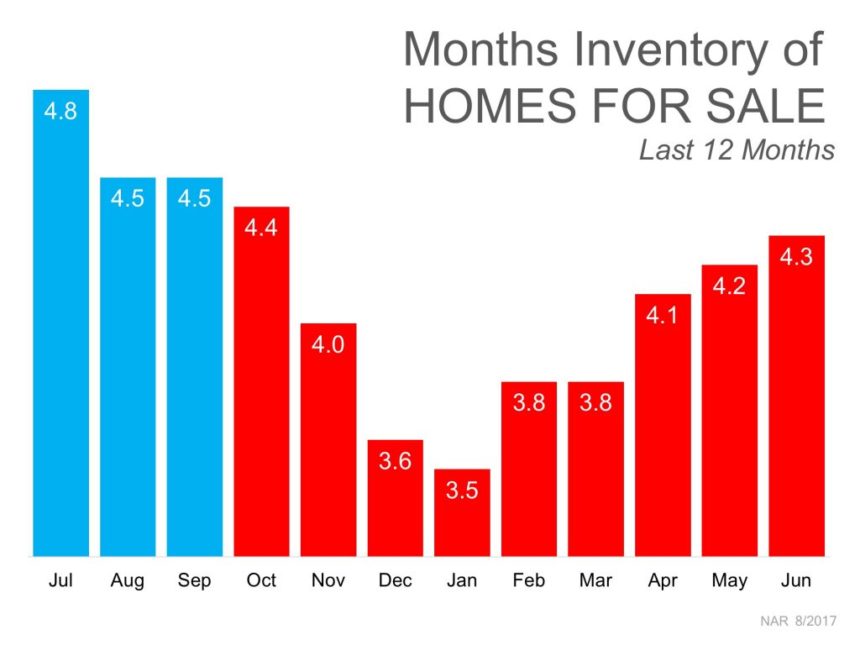

The most recent Months Supply of Inventory numbers show that supply is nowhere near meeting the demand:

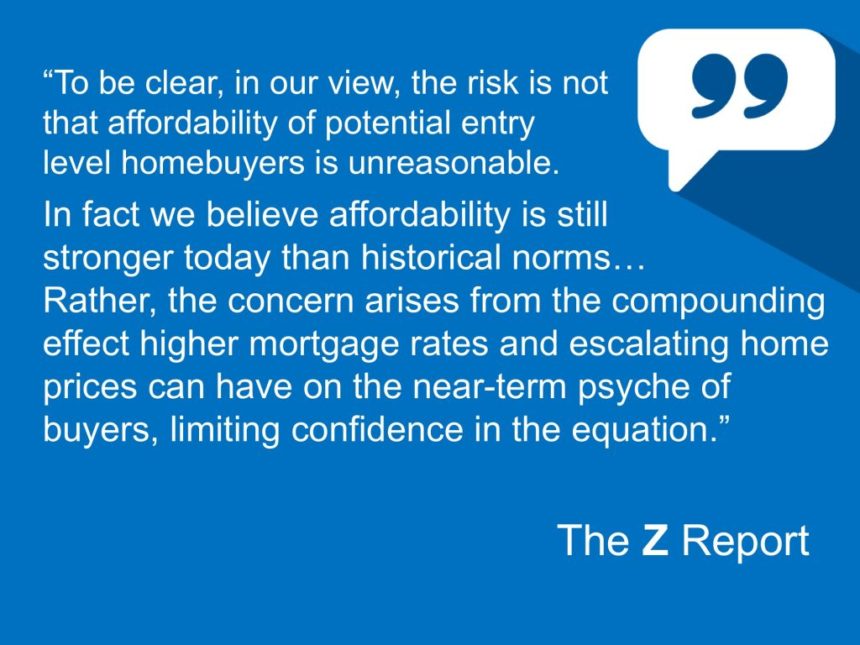

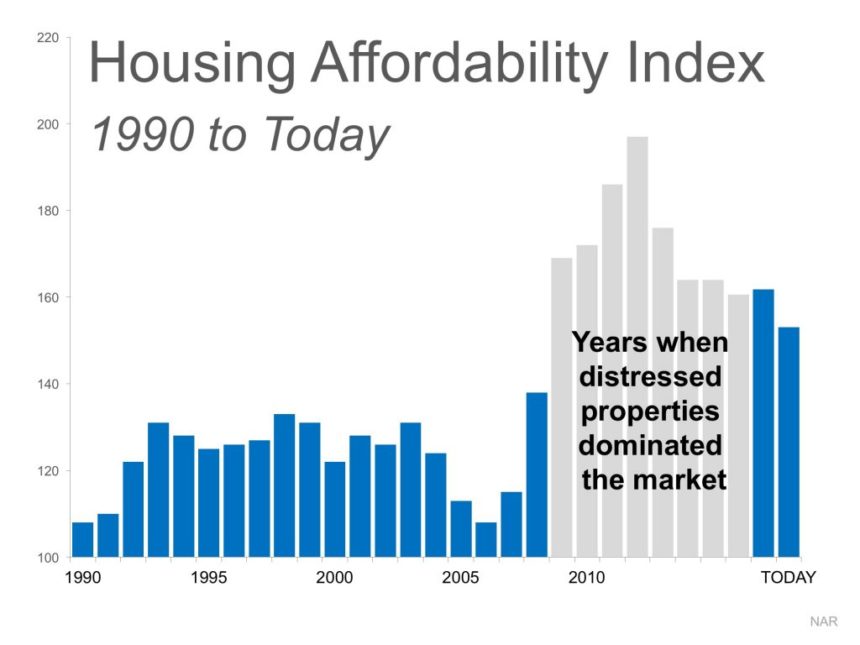

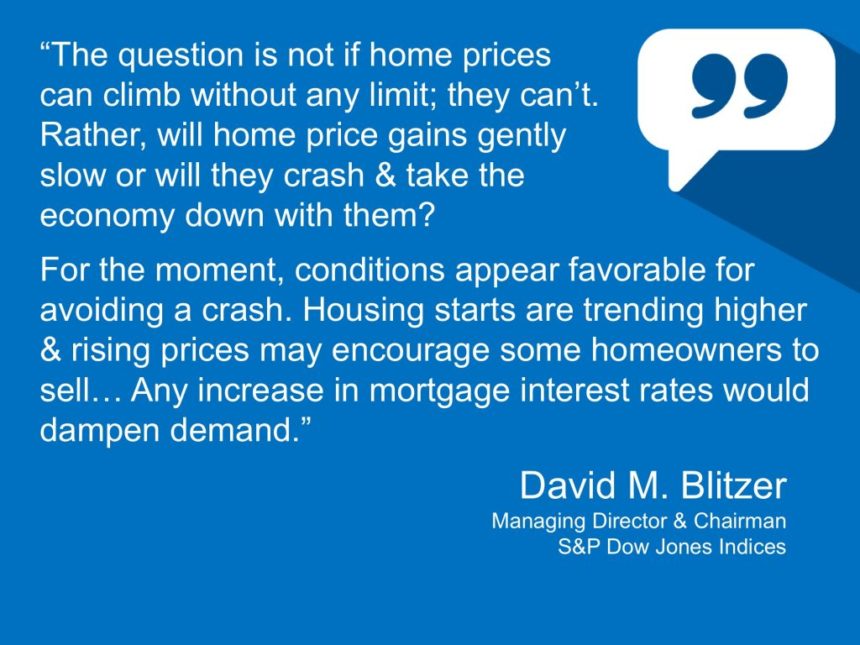

Would be buyers staying out of the market is a very real concern, as it was recently expressed by real estate guru Ivy Zelman:

One thing she touched on in that quote was affordability.

Home affordability is the highest it has been in decades, despite rising prices.

So, demand is clearly not an issue with the current market. There simply are not enough homes available.

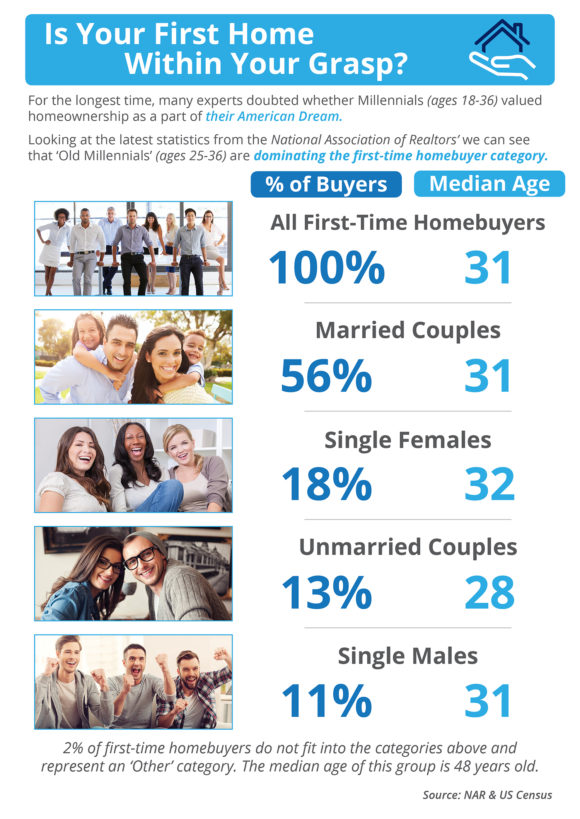

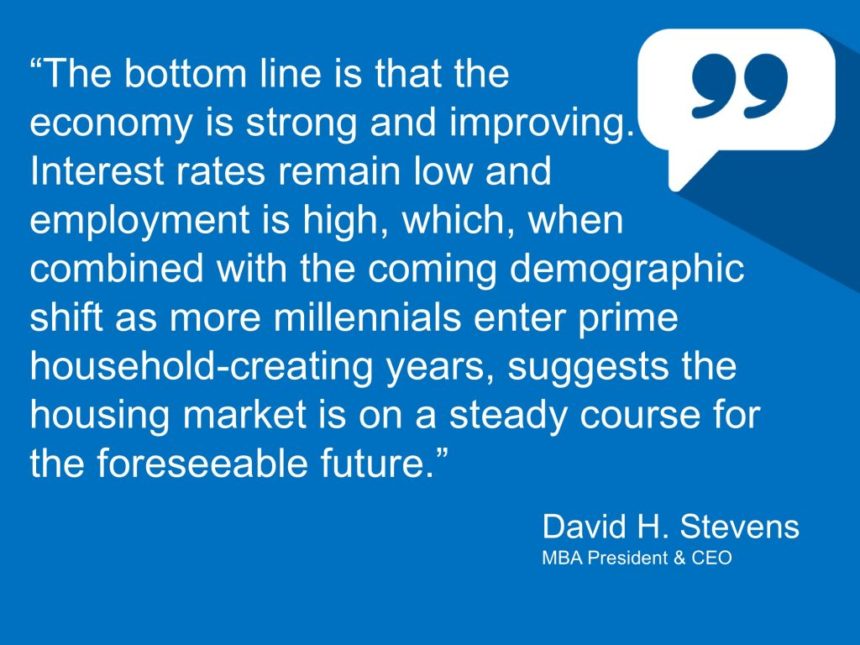

5. The Millennials

The Millennial generation makes up the largest portion of our population.

They have entered the real estate market in the last few years, and their impact has been felt.

In fact, they make up the largest segment of first time home buyers:

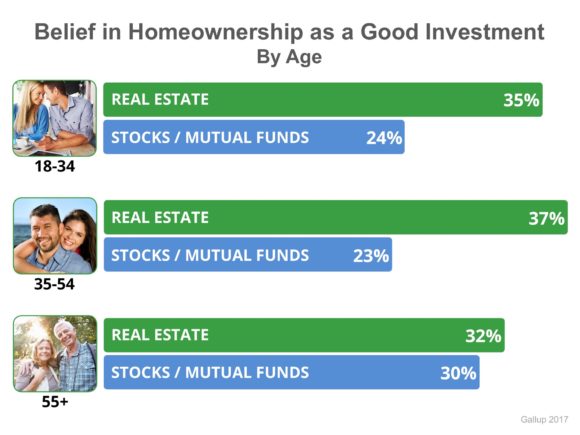

Millennials also value the goal of home ownership:

Current Millennial home buyers are comprised mostly of the “Old Millennials”, ages 25-36.

So this leaves a large population of future demand that will be entering the housing market in the coming years.

In other words, we have just scratched the surface of an entirely new wave of buyers and sellers.

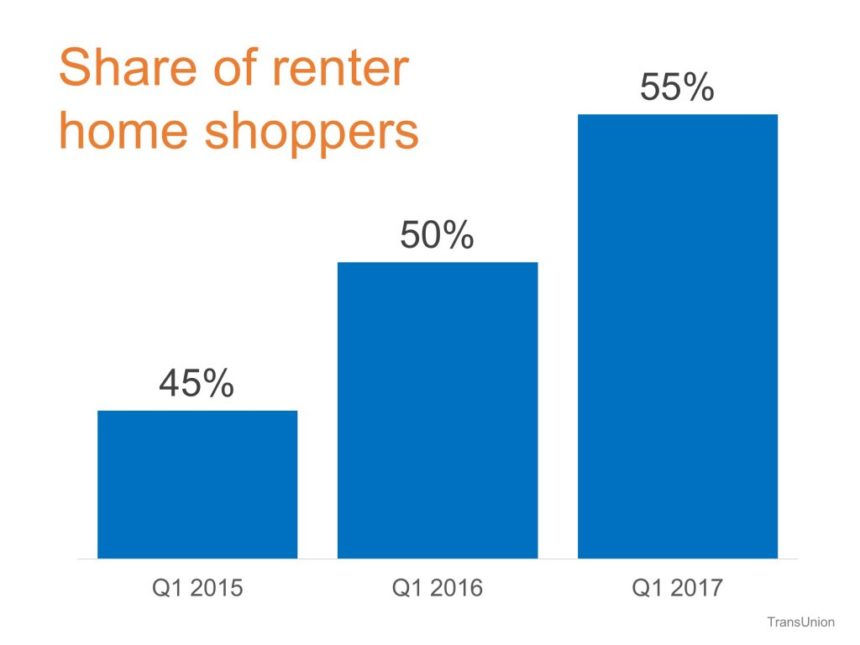

6. Rental Market

Not only has the residential home sale market heated up over the last few years, the rental market has also exploded.

Rents are rising sharply, and inventory is also a major issue.

More and more renters are recognizing that it makes better financial sense to own as opposed to renting.

More renters are entering the real estate market, looking to purchase a home:

Renters are frustrated by rising rents, limited availability, and having to live by someone else’s rules.

They also realize that whether they are paying rent or own, either way they are paying someone’s mortgage.

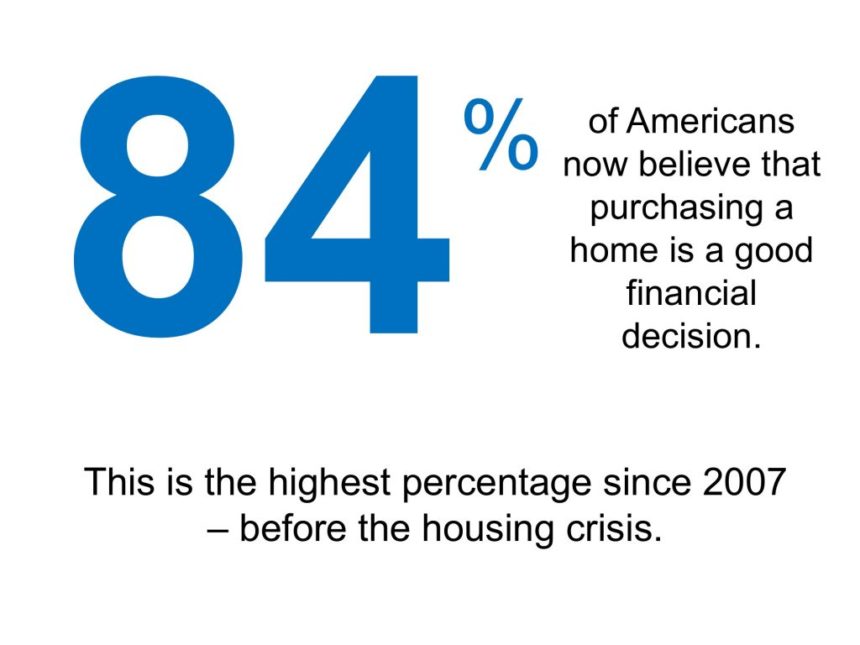

A recent report from the National Association of Realtors (NAR) shows that the majority of American’s consider home ownership a good financial decision:

What’s The Outlook For The Housing Market?

Demand is clearly not the issue. With a limited supply of homes, values look to continue to increase.

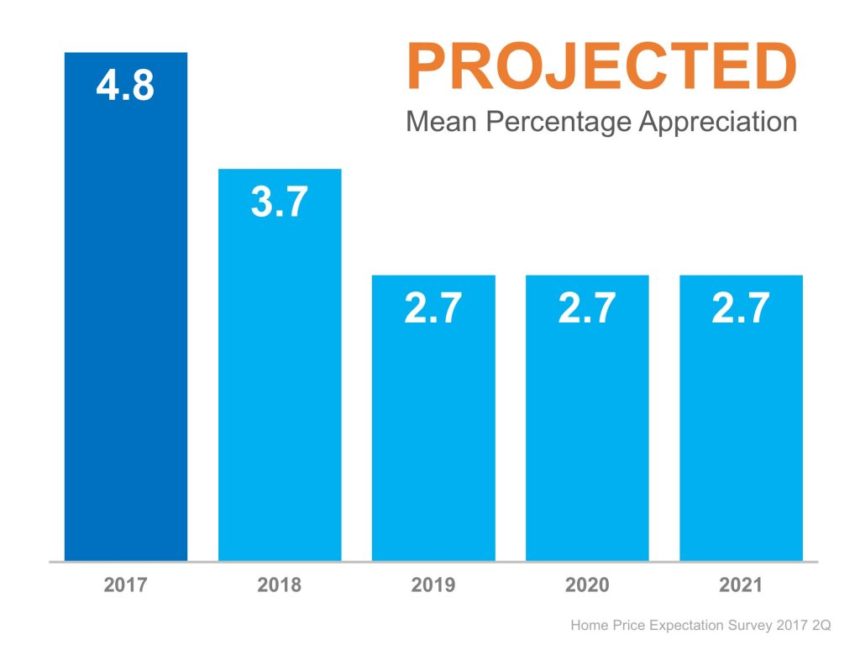

One resource to look at the future of home values is the latest Home Price Expectation Survey.

This is a quarterly survey of over one hundred economists, real estate experts and investment & market strategists to project home values over the next five years.

In the most recent survey, the experts predicted that houses would continue to appreciate through 2021.

They expect lower levels of appreciation during these years than we have experienced over the last five years.

However, they do not forecast a decrease in values (depreciation) in any of the upcoming years.

Of course, those that are predicting another housing bubble will say “what goes up, must come down”.

There is some truth to that statement, but it is not as simple as that:

So while there are important factors to keep an eye on as we head towards 2018, the experts aren’t hitting any panic buttons.

Be sure to visit my Pam Marshall Realtor website for more information about the real estate market.

You can follow the latest news, stats, and trends of the real estate market, nationally and here in Charleston, SC at this blog or this blog.

Follow me on Facebook and Twitter.

You can also download one of my free real estate guides:

Leave a Reply